The prioritization model listed in a Portfolio Strategic Plan guides how the portfolio management practice will sort, select, and sequence initiatives. A model defines the criteria that express strategic intent, specifies how each criterion is measured, and assigns weights that reflect relative importance for the portfolio. The model provides a repeatable decision rule that portfolio managers and governing bodies can apply across projects, programs, or other initiatives.

Prioritization models usually combine criteria, scoring scales, and aggregation rules. Criteria describe dimensions such as strategic fit, financial contribution, risk exposure, regulatory obligations, capability development, and social or environmental impact. Scoring scales translate observed performance into numeric values, often using ordinal levels such as one to five or verbal anchors such as very low to very high. Aggregation rules then combine scores with weights, often through a weighted sum, to produce a priority index that supports ranking and grouping.

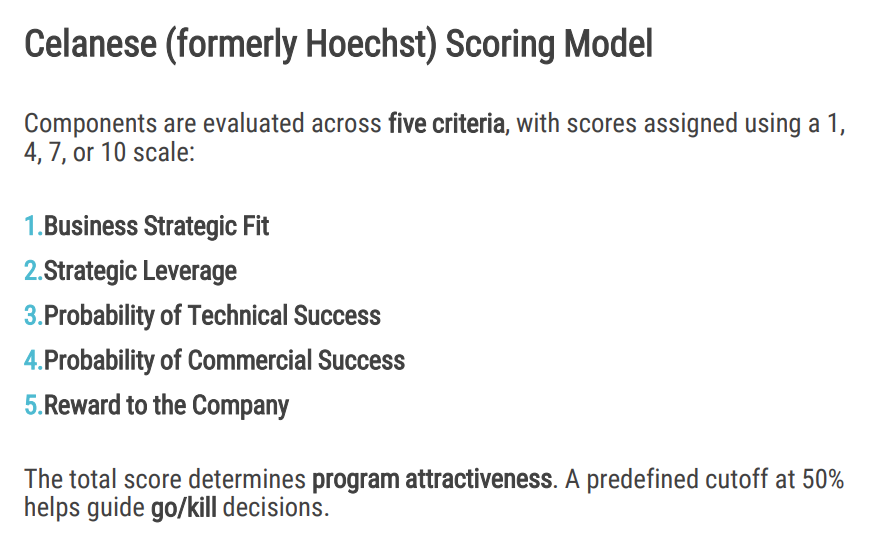

Example:

Scorecards serve as the operational interface of these models. A scorecard presents the criteria, scales, and weights in a structured template for each initiative. Evaluators record scores, the system calculates weighted totals, and portfolio discussions use these results to compare options and form shortlists. Many organizations adopt scorecards early in the strategic planning cycle to screen large sets of ideas, segment proposals into tiers, and focus advanced analysis on the most promising candidates. Scorecards can be used again in later stages to refine sequencing or to reassess items after new information emerges.

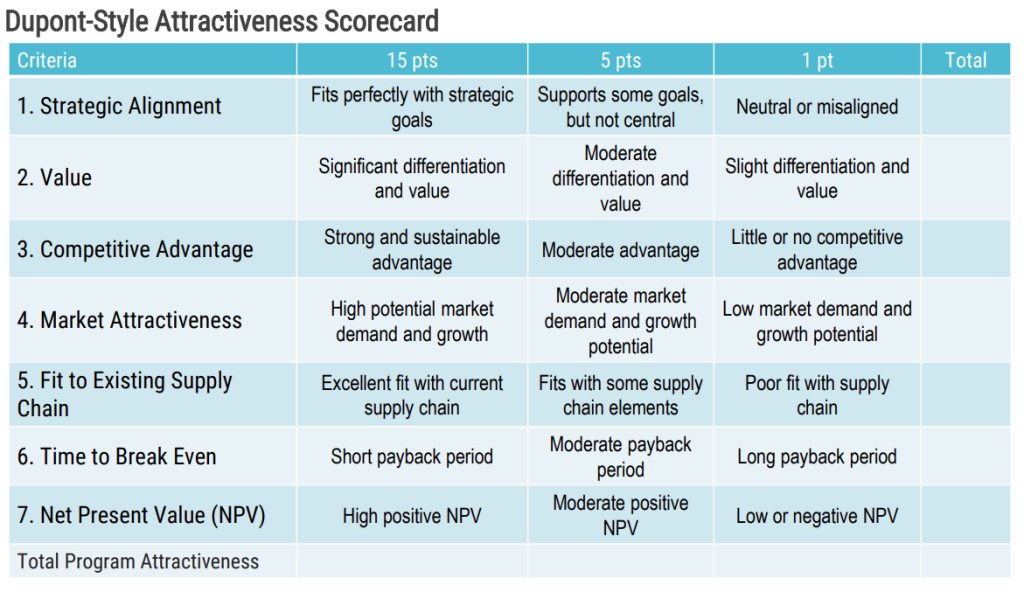

Example:

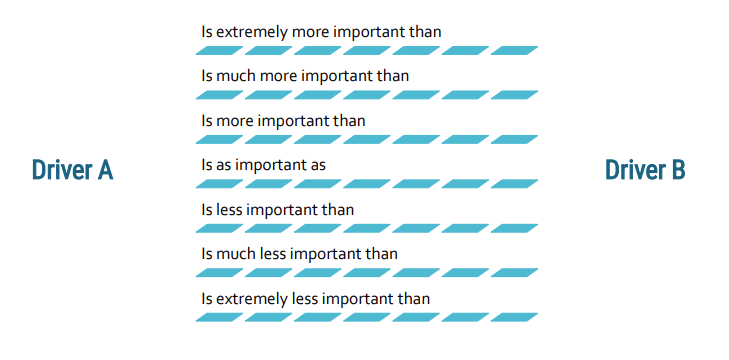

Analytic Hierarchy Process, or AHP, is a structured multi-criteria decision-making method that helps compare alternatives when several, often conflicting, factors matter. AHP first breaks a decision down into a hierarchy with the overall goal at the top, followed by criteria and sub-criteria, and alternatives at the bottom. Decision makers then perform pairwise comparisons, judging the relative importance of one element versus another using a numerical scale, which converts qualitative preferences and expert judgments into quantitative priority weights. AHP checks the internal consistency of these judgments and aggregates the resulting weights through the hierarchy to produce an overall priority score for each alternative, supporting transparent and logically organized decisions in complex settings. Click here for a step by step look at AHP.

Fuzzy AHP adapts this approach for uncertainty in expert judgment. Instead of precise numbers, experts use fuzzy numbers or ranges to express preferences, which is useful when data are incomplete or when experts hesitate to give crisp ratios. Mathematical procedures then derive fuzzy weights and defuzzified point estimates that can populate scorecards, while preserving information about uncertainty in the underlying judgments.

AHP–Goal Programming hybrids link prioritization models with explicit resource and policy constraints. In these approaches, AHP generates weights and sometimes performance scores, while Goal Programming uses those inputs along with constraints such as budget, capacity, or risk limits. The optimization then selects a set of projects that meets or approximates multiple targets, such as minimum aggregate benefit, maximum acceptable risk, or balanced allocation across strategic themes. Scorecards provide the structured evaluation data that feed these optimization models.

Recent work on project portfolio selection emphasizes integrated and hybrid methods that go beyond basic scoring. Some models combine Quality Function Deployment, fuzzy logic, and Data Envelopment Analysis to handle criterion prioritization, uncertainty, and project interdependencies in a single framework. Other approaches integrate AHP with simple additive weighting, event tree scenario analysis, or metaheuristic optimization to account for project combinations, interproject effects, and robustness of portfolios under different future states.

Research on ranking criteria in project portfolio management proposes families of dimensions that can be embedded in scorecards. Common groups include financial and economic value, strategic alignment, risk and uncertainty, resource requirements, stakeholder and customer impact, learning and innovation, and sustainability. Studies highlight the need to translate high-level strategic objectives into concrete, measurable criteria so that scorecards act as a bridge between strategy and individual investment decisions.

Multi-criteria decision-making techniques play a central role in modern prioritization models. Beyond AHP and fuzzy AHP, organizations use TOPSIS, additive ratio assessment methods, interactive methods such as TODIM, and probability models such as Bradley–Terry. These techniques support different preference formats, from pairwise comparisons to direct ratings or rankings, and help merge qualitative assessments with quantitative data into consistent project rankings.

TOPSIS, or Technique for Order of Preference by Similarity to Ideal Solution, ranks alternatives based on their geometric distances from two reference points. The method defines a positive ideal solution that has the best observed performance on each criterion, and a negative ideal solution that has the worst observed performance. It then normalizes the decision matrix, applies weights, and computes the distance of each alternative to both ideal and anti-ideal points. The relative closeness index expresses how near each alternative is to the positive ideal and how far it is from the negative ideal, which supports a straightforward ranking of options by this closeness measure.

Variants of TOPSIS extend the basic idea to more complex settings. Fuzzy TOPSIS uses fuzzy numbers to model uncertain or linguistic assessments, and group TOPSIS aggregates evaluations from multiple decision makers into a single decision matrix. Recent robust and Bayesian versions treat weights, evaluations, or decision-maker preferences as random variables. Robust TOPSIS incorporates simulation and stochastic analysis to handle non-monotonic criteria and hierarchical structures. Bayesian TOPSIS treats the relative closeness scores as probabilistic quantities and uses hierarchical Bayesian models to aggregate preferences from a group, which reduces sensitivity to outliers in individual judgments.

Additive ratio assessment methods, commonly labeled ARAS, rank alternatives by comparing their weighted performance to an idealized reference. ARAS begins by constructing and normalizing a decision matrix that includes a hypothetical optimal alternative. The method then multiplies each normalized criterion value by its weight and sums these products to obtain a utility value for each alternative. The final utility degree expresses the ratio of each alternative’s performance to the ideal alternative, which provides both an absolute performance index and a relative ranking. This additive structure accommodates benefit and cost criteria through appropriate normalization and sign conventions.

Modern ARAS applications often integrate objective and subjective weighting schemes and fuzzy or intuitionistic fuzzy representations of data. Some studies combine entropy, CRITIC (see below), or other objective weighting methods with expert-based weights to derive composite importance coefficients for each criterion. Others embed ARAS inside hybrid frameworks that use fuzzy sets, picture fuzzy sets, or other uncertainty formalisms. In these designs, ARAS operates on transformed or aggregated evaluations while preserving the core idea of additive utility ratios relative to an ideal solution, which makes the method suitable for ranking projects, risks, or policy options.

CRITIC is a weighting method that derives objective criterion weights from the structure of the evaluation data. The name CRITIC stands for “CRiteria Importance Through Intercriteria Correlation.” The procedure starts from a decision matrix and first measures the contrast intensity of each criterion, often using the standard deviation of its values across alternatives. A criterion with higher variability has greater discriminating power among alternatives and thus receives a higher raw importance score from this component. The method then computes the correlations between each pair of criteria. A criterion that is highly correlated with many others adds less unique information, whereas a criterion with low correlations contributes more independent information.

The final CRITIC weight for a criterion combines contrast intensity and conflict with other criteria. For each criterion, the method multiplies its standard deviation by a term that reflects the sum of one minus the absolute correlation with all other criteria. This product captures both how strongly the criterion separates alternatives and how distinct the criterion is from the rest. Normalizing these products across all criteria yields a weight vector that gives more influence to criteria that vary widely across alternatives and that carry nonredundant information. Because CRITIC uses only the properties of the data, the method provides an objective complement to subjective weighting approaches based on expert judgment.

Recent decision models often combine CRITIC with TODIM (see below) to obtain hybrid subjective–objective weights. In these models, CRITIC supplies an objective weight component that reflects the informational structure of the criteria, and another method such as the Best–Worst Method or entropy scoring provides a subjective component based on decision maker preferences. The combined weights then feed into TODIM’s dominance calculation, which uses prospect theory to account for risk perception and loss aversion. This integration helps construct multi‑criteria decision procedures that reflect both behavioral attitudes and data‑driven importance patterns in applications such as network security team evaluation, stock investment selection, electric vehicle choice, FinTech startup assessment, and credit risk analysis in supply chain finance.

TODIM is a behavioral multi‑criteria decision method that models how people perceive gains and losses. The name TODIM comes from the Portuguese phrase “TOmada de Decisão Interativa e Multicritério,” which translates to “Interactive and Multi‑criteria Decision Making.” The acronym signals two design ideas: the method supports interaction among decision makers, and the method evaluates alternatives across multiple criteria at the same time, rather than through a single performance measure.

The core objective of TODIM is to rank alternatives using a dominance function derived from prospect theory. The method begins with a decision matrix that records the performance of each alternative on each criterion and with a weight vector that expresses the relative importance of criteria. TODIM selects a reference criterion or constructs a reference point and then compares each pair of alternatives on every criterion. For each comparison, the method calculates a gain or a loss relative to the reference and transforms this difference through value functions that have different shapes for gains and for losses. Losses usually receive a steeper penalty than equivalent gains receive rewards, in line with loss aversion. Summing these transformed differences across criteria yields a dominance degree for each ordered pair of alternatives, and aggregating dominance degrees over all comparisons produces an overall dominance score and a ranking.

Prospect theory gives TODIM its behavioral meaning. Prospect theory assumes that decision makers evaluate outcomes relative to a reference point, that they feel losses more strongly than gains of the same magnitude, and that sensitivity to changes decreases for larger absolute outcomes. TODIM encodes these features by defining separate value functions for gains and losses and by using a loss aversion parameter in the loss function. A higher loss aversion parameter produces dominance scores that penalize alternatives with potential losses more strongly. This structure lets TODIM emulate observed risk attitudes in domains such as stock selection, emergency response, green supplier choice, and geopolitical risk evaluation.

Extensions of TODIM adapt the original algorithm to more complex data and interaction patterns. Fuzzy TODIM variants use intuitionistic fuzzy sets, Pythagorean fuzzy sets, picture fuzzy sets, or probabilistic dual hesitant fuzzy sets to represent uncertain and imprecise evaluations. Some models incorporate the Choquet integral to handle interactions among criteria and to derive Shapley value–based weights for interdependent attributes. Other work integrates cumulative prospect theory explicitly, producing CPT–TODIM versions that recast the dominance calculation in terms of cumulative decision weights and probability distortions. Generalized forms of TODIM simplify the dominance function and establish conditions for weight consistency and weight monotonicity, which align the method’s behavior with intuitive expectations about the impact of changing criterion weights.

Probability models such as Bradley–Terry provide a different way to prioritize alternatives using pairwise comparison data. The Bradley–Terry model assumes that each alternative has an underlying positive parameter that represents its latent “strength” or preference value. When two alternatives are compared, the probability that one is preferred over the other equals its strength divided by the sum of both strengths. By observing many pairwise comparisons, the model estimates these strength parameters using maximum likelihood or Bayesian methods. The resulting parameter estimates induce a natural ranking of alternatives that reflects the probabilities of winning in pairwise contests.

Recent applications of Bradley–Terry models link them directly to multi-criteria structures such as the Balanced Scorecard. In these contexts, decision makers perform structured pairwise comparisons of strategic drivers, projects, or criteria, and the model estimates strength parameters for each element. These parameters serve as preference weights or priority scores that can feed into broader portfolio decision frameworks. Probabilistic extensions allow the model to incorporate uncertainty and heterogeneity in decision makers’ responses. By framing prioritization as a stochastic process over pairwise choices, Bradley–Terry models offer an analytically transparent way to derive rankings from discrete judgment data rather than from direct scoring of alternatives.

Newer contributions focus on practical issues such as reducing cognitive load for experts, increasing consistency, and integrating heterogeneous evaluation formats. Hybrid AHP variants reduce the number of comparisons while preserving rankings. Multimethod approaches provide mappings that allow portfolios evaluated with different methods and preference formats to be merged and reprioritized in a unified scheme. Literature reviews also stress the design of criteria and the early-stage filtering of criteria themselves, not only the ranking of projects, as a distinct methodological problem.

References:

- “A methodology for project portfolio selection under criteria prioritisation, uncertainty and projects interdependency – combination of fuzzy QFD and DEA” – Hamed Jafarzadeh, Pouria Akbari, Baharom Abedin

- “Prioritization of project proposals in portfolio management using fuzzy AHP” – Kajal Chatterjee, Sheikh A. Hossain, Suman Kar

- “SCIENTIFIC APPROACHES TO PRIORITIZATION OF INVESTMENT PROJECT PORTFOLIO AT INFRASTRUCTURE ENTERPRISE” – Volodymyr Shemayev, Polina Tolok

- “A Bradley-Terry Model-Based Approach to Prioritize the Balance Scorecard Driving Factors: The Case Study of a Financial Software Factory” – Víctor Rodríguez Montequín, Joaquín Villanueva Balsera, Marta Díaz Piloñeta, César Álvarez Pérez

- “Multimethod to prioritize projects evaluated in different formats” – Fernando Ramalho, Iara Sibele Silva, Pedro Ekel, Carlos Denner dos Santos Martins, Patrícia Bernardes, Marconi Libório

- “integrative review of project portfolio management ranking criteria – understanding better the decision-making process” – Patrícia Pionório, Zoltán Sebestyén

- “The use of multi-criteria decision-making methods in project portfolio selection: a literature review and future research directions” – Mehmet Kandakoglu, Saoussen Ben Amor

- “Using the deterministic approach model for project portfolio selection problem (PPSP) solutions” – Abiodun Mogbojuri, Olukayode Olanrewaju

- “Fuzzy portfolio selection using fuzzy analytic hierarchy process” – Funda Tiryaki, Burcu Ozkok

- “Analytical hierarchy process: revolution and evolution” – Madjid Tavana, Mohammad Soltanifar, Francisco Santos-Arteaga

- “A comprehensive guide to the TOPSIS method for multi-criteria decision making” – Mitra Madanchian, Hamed Taherdoost

- “Application of TOPSIS for Multi-Criteria Decision Analysis (MCDA) in Power Systems: A Systematic Literature Review” – Jack Mathebula, Nhlanhla Mbuli

- “A robust TOPSIS method for decision making problems with hierarchical and non-monotonic criteria” – Salvatore Corrente, Menelaos Tasiou

- “A reliable probabilistic risk-based decision-making method: Bayesian Technique for Order of Preference by Similarity to Ideal Solution (B-TOPSIS)” – He Li, Mohammad Yazdi, Cheng-Geng Huang, Wei Peng

- “Additive Ratio Assessment Method (ARM/ARAS)” – Jitesh Thakkar

- “Towards Sustainable Development: Ranking of Soil Erosion-Prone Areas Using Morphometric Analysis and Multi-Criteria Decision-Making Techniques” – Padala Raja Shekar, Aneesh Mathew, Fahdah Falah Ben Hasher, Kaleem Mehmood, Mohamed Zhran

- “Digital transformation project risks assessment using hybrid picture fuzzy distance measure-based additive ratio assessment method” – Pratibha Rani, Anupam Mishra, A. F. Alrasheedi, Dragan Pamucar, Dragan Marinković

- “Intuitionistic fuzzy fairly operators and additive ratio assessment-based integrated model for selecting the optimal sustainable industrial building options” – Anupam Mishra, Pratibha Rani, Francesco Cavallaro, Ibrahim M. Hezam

- “An analysis of the generalized TODIM method” – Beatriz Llamazares

- “An extended TODIM approach with intuitionistic linguistic numbers” – Su-min Yu, Jing Wang, Jian-qiang Wang

- “A Picture Fuzzy Multiple Criteria Decision-Making Approach Based on the Combined TODIM-VIKOR and Entropy Weighted Method” – Vikas Arya, Satish Kumar

- “AN INTEGRATED PICTURE FUZZY ANP-TODIM MULTI-CRITERIA DECISION-MAKING APPROACH FOR TOURISM ATTRACTION RECOMMENDATION” – Chao Tian, Juan-juan Peng

- “Multi-Criteria Decision-Making Method Based on Distance Measure and Choquet Integral for Linguistic Z-Numbers” – Jian-qiang Wang, Yong-xi Cao, Hong-yu Zhang

- “Prioritization of policy initiatives to overcome Industry 4.0 transformation barriers based on a Pythagorean fuzzy multi-criteria decision making approach” – Detcharat Sumrit

- “Sustainability diet index: a multi-criteria decision analysis proposal for culinary preparations—a case study” – Rodrigo Contreras-Núñez, Andrea Espinoza, Paola Cáceres

- “Behavioral multi-criteria decision analysis: the TODIM method with criteria interactions” – Luiz Flávio Autran Monteiro Gomes, Maria Augusta Soares Machado, Luiz Flávio Rangel

- “An extended TODIM multi-criteria group decision making method for green supplier selection in interval type-2 fuzzy environment” – Jindong Qin, Xinwang Liu, Witold Pedrycz

- “Pythagorean fuzzy TODIM approach to multi-criteria decision making” – Peijia Ren, Zeshui Xu, Xunjie Gou

- “Extended TODIM method for multi-attribute risk decision making problems in emergency response” – Mingyang Li, Ping-Ping Cao

- “TODIM method based on cumulative prospect theory for multiple attribute group decision-making under 2-tuple linguistic Pythagorean fuzzy environment” – Yangjingyu Zhang, Guiwu Wei, Yanfeng Guo, Cun Wei

- “TODIM method based on cumulative prospect theory for multiple attributes group decision making under probabilistic hesitant fuzzy setting” – Ningna Liao, Guiwu Wei, Xudong Chen

- “Extension of intuitionistic fuzzy TODIM technique for multi-criteria decision making method based on Shapley weighted divergence measure” – Pratibha Rani, D. Jain, D. S. Hooda

- “An extended TODIM method for hesitant fuzzy interactive multicriteria decision making based on generalized Choquet integral” – Chunqiao Tan, Zhong-Zhong Jiang, Xiao-hong Chen

- “TODIM-based multi-criteria decision-making method with hesitant fuzzy linguistic term sets” – Mingwei Lin, Huibing Wang, Zeshui Xu

- “Improved TODIM method for intuitionistic fuzzy MAGDM based on cumulative prospect theory and its application on stock investment selection” – Mengwei Zhao, Guiwu Wei, Cun Wei, Jiang Wu

- “TODIM method for multiple attribute group decision making based on cumulative prospect theory with 2-tuple linguistic neutrosophic sets” – Mengwei Zhao, Guiwu Wei, Jiang Wu, Yanfeng Guo, Cun Wei

- “A Novel Multi-Criteria Quantum Group Decision-Making Model Considering Decision Makers’ Risk Perception Based on Type-2 Fuzzy Numbers” – Wen Li, Shuaicheng Lu, Zhiliang Ren, Omer Rehman

- “A Novel Interval Type-2 Fuzzy CPT-TODIM Method for Multi-criteria Group Decision Making and Its Application to Credit Risk Assessment in Supply Chain Finance” – Wen Li, Luqi Wang, Omer Rehman

- “Improved TODIM Method for Probabilistic Linguistic MAGDM Based on New Distance Measure” – Ke Li, Lei Xu, Yi Liu, Hongjuan Wang, Yuan Rong

- “An Enhanced Interactive and Multi-criteria Decision-Making (TODIM) Method with Probabilistic Dual Hesitant Fuzzy Sets for Risk Evaluation of Arctic Geopolitics” – Chenyang Song, Zeshui Xu, Yixin Zhang

- “Choquet based TOPSIS and TODIM for dynamic and heterogeneous decision making with criteria interaction” – Rodolfo Lourenzutti, Rafael H. N. Krohling, Marek Reformat