In Project Management, the “PMI way,” we address two type of reserves, the contingency reserve which is the budget set aside to cover potential costs for things that are identified as possible risks to the project. It provides funding to address known-unknowns – risks that have been identified and analyzed, and we know how much it will cost us if these risks materialize. Contingency reserves are intended to cover uncertainties that can be reasonably forecasted.

The second type of reserve is the management reserve. The management reserve is budget withheld for unforeseen work that was entirely unidentified in project planning stages. It covers unknown-unknowns – issues that arise that were completely unexpected and had not been assessed as project risks. For the PMP test, you can assume that the project sponsor holds the management reserve.

The management reserve is set aside to provides the project with additional funding flexibility to handle emergent scope or needs: The surprises that we didn’t see coming but are in-scope for our project to address.

In summary:

Contingency reserve is for identified risks that were planned for. Management reserve is for unidentified issues that arise unexpectedly.

In the PMBOK guide 7th edition, the definition of cost baseline was updated to the following:

“The cost baseline is the approved version of the time-phased project budget, excluding any management reserves, which can only be changed through formal change control procedures. It is used as a basis for comparison to actual results.”

Historically when creating a cost baseline, PMI recommended including your contingency reserve (to cover the cost of the known unknowns). I consider this money saved for a rainy day, and an example, can be just that: if it rains (risk), for Activity A we will need to spend $250 on umbrellas. As each activity is reviewed for risk, a contingency can be added: “Oh, for Activity B, If Bella is unavailable that week for whatever reason, we will need to pay a partner company to do it and it will cost an extra $300″). At the end of this post you can see an example of why a PM might wish to add a contingency reserve to the work package level. For now, I just want to address “the PMI way” (circa 2023) and how you can manage your projects like a Rockstar knowing this information.

Including the contingency reserve in the cost baseline — which would then become the approved cost baseline –made lots of sense because I know if it rains I need $250 for umbrellas, why should I have to ask someone for this money (e.g. via the process of integrated change control)?

So that was fine… Until the PMBOK 7 came out, and one of the diagrams therein showed the contingency reserve sitting atop the cost baseline. This confused lots of people, but in the end (and by “end” I mean July 2023) we know that PMI does want you to add those contingency reserves into the cost baseline. (This is something that was communicated to authorized PMP test prep instructors like myself, and something that all PMP Test Prep students will see in their downloadable test prep slides, etc.)

PMI when PMP test prep students try to look this up in the PMBOK 7:

(There is a graphic in your PMBOK7, but don’t use that one — PMI is back to promoting the version we saw in PMBOK6 and prior)

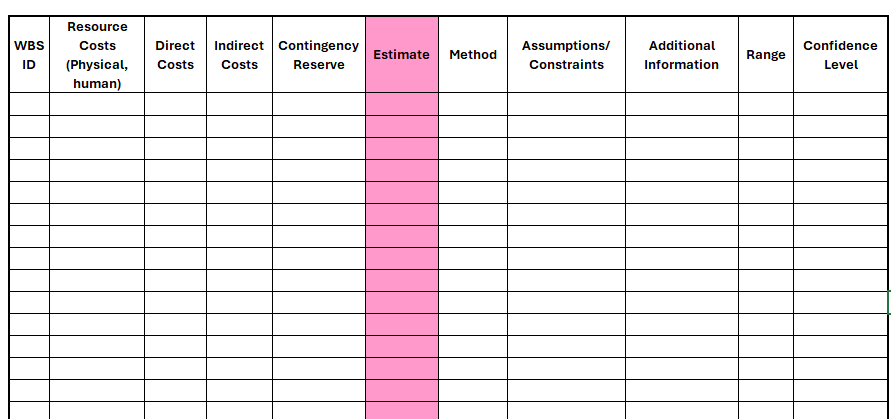

What does this mean in a practical sense? Lets talk risk management. Your Risk Management Plan is a comprehensive plan that tells you all the HOWS (and the WHOs and the WHATs and WHENs) as they relate to identifying and assessing project risks, including how to come up with estimated costs associated with each risk. Using this plan and your activity cost estimates spreadsheet — surrounded by your team and maybe a SME (subject matter expert) or two — you would note any applicable contingencies for affected activities… These would be in their own column of your activity cost estimate spreadsheet. The aggregate of these contingencies would be the basis for the contingency reserve. (You might add in more contingencies at the WP level as you flesh out the true reserve that you need.)

Now, as much as I like the idea of getting the money I set aside for a rainy day when it rains (without jumping through hoops, you know… in the rain), if I truly added the contingency reserve to my time-phased budget (S-curve) when tracking project performance during project execution, it would obscure my EVM (Earned Value Management). I’d look like a Rockstar but I might be eating into rainy day money when I shouldn’t be.

So here’s the finer points that are often missed:

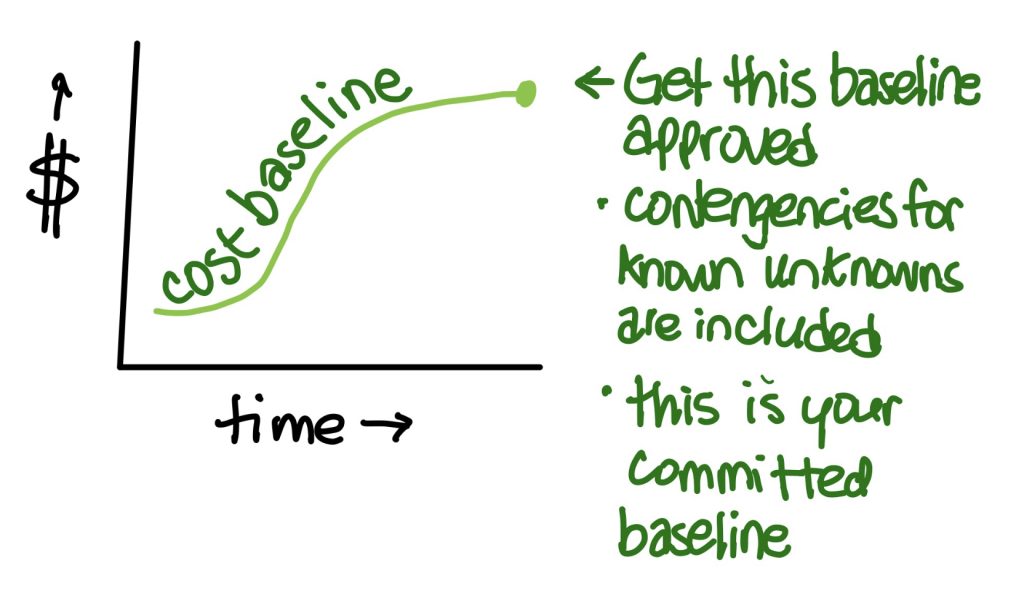

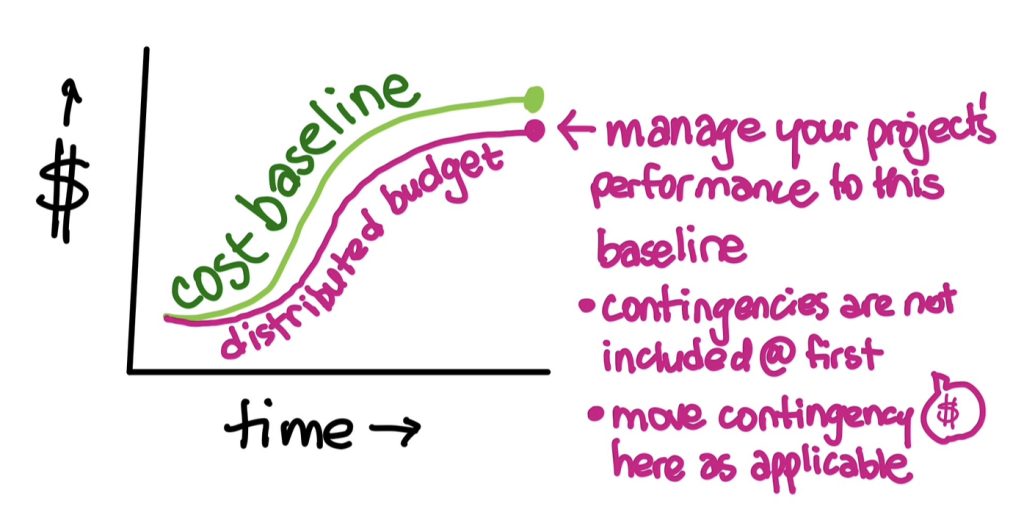

During the planning phase, the project manager develops the cost baseline, which includes the cost estimates for activities (resource costs, direct and indirect costs, etc), plus all of the identified contingencies for known risks (found for activities and for work packages). This Cost Baseline might be presented as an S-curve and is typically what gets approved by project stakeholders.

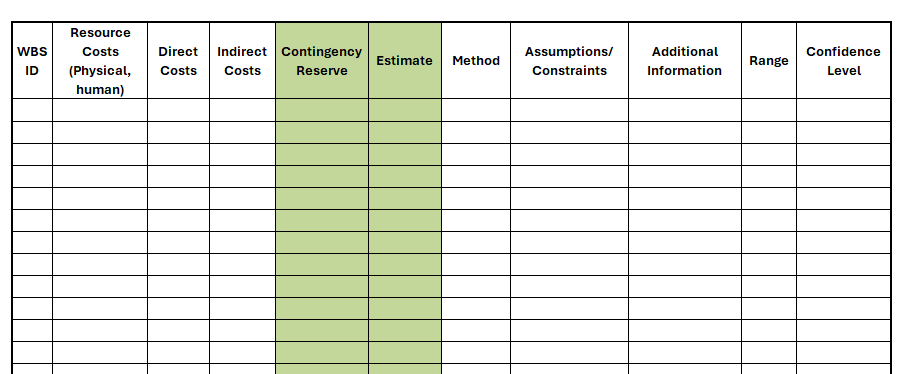

The above S-curve is based on aggregating all the $ listed in the 2 columns below (plus WP-level contingencies which are not shown):

NOTE: The spreadsheet above is the Activity Cost Estimate spreadsheet. Not shown are the columns for the activity name, activity ID, and brief description/notes. These columns are also cut off in the subsequent image.

Then, during project execution, the project manager uses the Performance Measurement Baseline (PMB), which excludes the contingency reserves. The PMB is used to track and measure the project’s performance over time. This provides a more accurate reflection of the project’s actual performance, as it doesn’t include funds set aside for those rainy days. The PMB includes scope, schedule, and cost baselines. It’s used to compare actual project performance against what was planned (see my GIF below ♫You’re all about that base[line], that base[line], that base[line]…♫).

The pink curve above is based on the aggregate of the estimates, without adding in the contingency reserve:

The portion of the PMB that relates to cost can be called the distributed budget. In other words, my time-phased budget that I and the team would track our performance against would be representing the distributed budget. The distributed budget is the core cost estimate total for all work packages and control accounts. We are NOT considering the contingencies here. (Again, if reserves are built into the distributed budget, it obscures EVM performance measurement.)

However, the cost baseline does include the contingency reserve to the distributed budget to account for known-unknown risks.

Why do it this way? There are several advantages to this approach:

- EVM metrics are intended to measure performance against the distributed budget only, not reserves.

- Reserves should be incorporated into the overall budget but tracked and managed separately from the activities. (If reserves are part of the distributed budget, it would obscure EVM performance measurement.)

- Reserves are transferred into your distributed budget when needed (justified). This approach allows PMs to control the cost baseline with contingencies while keeping EVM focused on the core estimates (and appropriate adjustments made as risks materialize).

- The Project Manager’s authority often extends to managing the cost baseline only, not unallocated management reserves.

You Forgot Management Reserve

No I didn’t. A standard practice is to allocate management reserve as a percentage of the total budget, such as 5-10%. The higher the project risk, the higher the reserve percentage. The project sponsor is likely the one in charge of the management reserve.

(The sponsor likely controls the Management Reserve. If you need some of it, create your change request.)

Good New Though, as PM’s are… All About That Base, That Base, That Base….

(You’re all about that base, that base, that base — the 3 baselines: cost baseline, scope baseline, and schedule baseline… Oh an when executing, you’ll report on all three in a performance baseline)

Here’s What You’re Looking At:

- For each activity you have the activity cost estimate + contingency (two separate columns in yer spreadsheet)

- Additionally you may need to + contingency at the WP level

- Add all cost estimates up = distributed budget (you’ll manage your actual cost performance against this — PMI doesn’t use this term, but I add it here because it only makes sense to track EVM against this budget, and PMI does ❤️ EVM)

- Add all contingencies up = contingency reserve

- Distributed budget + contingency reserve = cost baseline

- Cost baseline + management reserve = project budget

When a Known Risk Materializes

For contingency reserves that were quantified for specific risks at the control account level during planning, the Project Manager often has the authority to transfer these reserves into the impacted control account budgets without full change control.

For example:

- In Control Account 1, a $5,000 risk was identified during planning. This amount is incorporated into the account’s budget as a contingency reserve.

- The risk materializes, requiring the control account’s budget to be increased.

- Since this risk was already quantified and accepted in the approved baseline, the contingency reserve of $5,000 is already incorporated into Control Account 1’s budget. If the risk materializes, the project manager has the authority to use these funds to address it.

- The PM documents the use of funds for tracking purposes but does not need additional approval. Diligent documentation is still needed for visibility and governance. The WBS dictionary, schedule docs, resource plans, and schedule forecasts would all need to stay synchronized with any work package or control account budget updates related to reserve usage. This would follow your configuration management system (versioning rules) as you are simply bringing documentation up to date to align with approved contingency execution. Updating these documents to reflect contingency reserve usage should fall under configuration management processes rather than requiring formal change control.

- Earned value performance metrics will then be measured against this updated distributed budget. Fair is fair.

Why Use a Contingency Reserve at the Work Package Level in Addition to (or Instead of) on my Activities?

A contingency reserve at the work package level is allocated to address known risks and uncertainties that apply to the entire work package. Let’s say your work package is Exterior Facade. After conducting a risk analysis for the entire Exterior Façade work package, you identify a critical risk related to the fluctuating prices of specialized glass panels required for the façade. Based on the trends in fluctuations you are looking at, you decide to allocate a cost contingency reserve of $15,000 to the work package.

The individual activities within the work package, such as installation of façade panels, labor costs, and other materials, are estimated based on their specific requirements and expected resource consumption. These activities may have their own risks associated (and thus their own contingencies applied), however the fluctuating specialized glass pricing only affects the work package level, so that is where this particular contingency is applied.

Good Risk Template Source: (Free)

https://www.vertex42.com/ExcelTemplates/risk-assessment-matrix.html